”It is not the strongest of the species that survive, nor the most intelligent, but the one most responsive to change.”

– Charles Darwin

Last week the market posted its best week of 2022 after seven straight weeks of losses, the longest losing streak since 2001. Through month-end, year to date, the S&P 500 was still down -13.04%.

Inflation Update

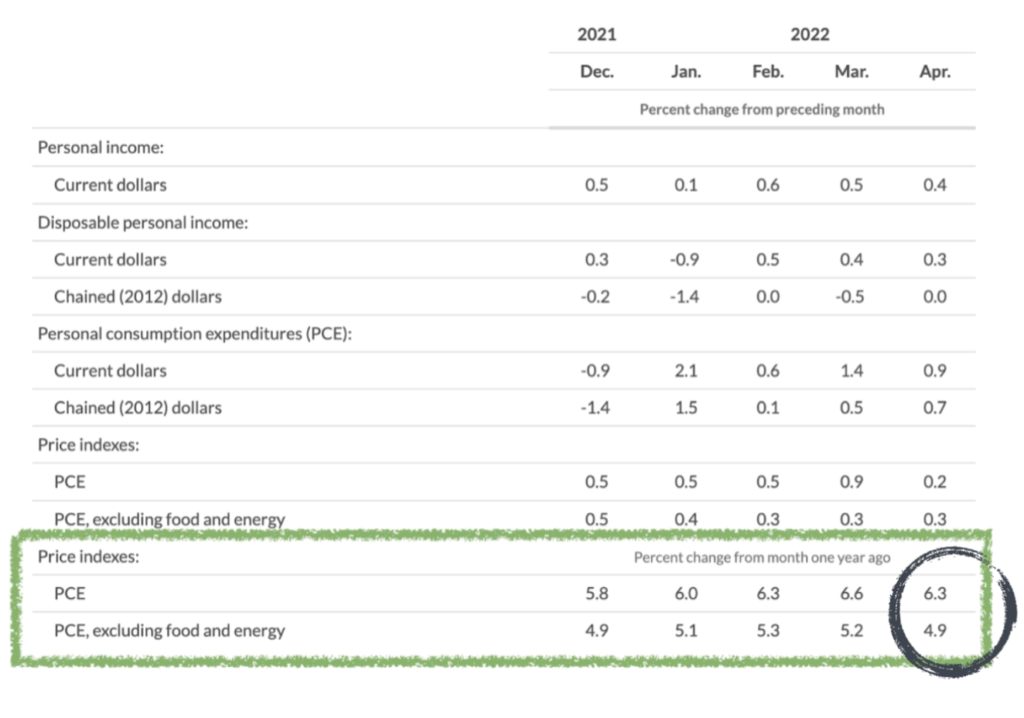

In the prior week, we also got the April PCE data. The index measures price changes across a variety of goods and services. The broadest measure of prices which includes food and energy rose at a 6.3% year-over-year pace in April compared to a 6.6% year-over-year pace in March. While prices were still rising most were happy that the rate prices were rising had slowed some (6.6% annualized vs 6.3% annualized). The Fed measures inflation by looking at core PCE, that is PCE without food and energy prices. Food and energy are stripped out of the reading because they are often very volatile. This makes sense from a measurement point of view, but don’t lose sight of the fact that food and energy prices are extremely important to the health of the consumer and they have been rising rapidly since the start of the war.

Headlines suggested that this month-over-month decrease could be signaling that inflation is potentially rolling over was of the reasons for the market’s rally. We remain skeptical about inflation rolling over. Most people agree that inflation peaked on a rate of change basis during the March and April timeframe, as in we don’t expect inflation readings to accelerate from 6% to 7% to 8% in the coming months. That being said, even if inflation just holds steady at a 6% annualized rate, that is still unacceptable to the Fed from a policy perspective.

First off, a one-month change is not a trend. And elsewhere, excluding food and energy, yes, there is a two-month deflationary trend in place. But, food and energy remain THE sources of inflation right now, and the upward pressure from those two areas seems to be not only firmly in place, but increasing still. If food and energy prices stay elevated, they eventually feed into the prices of other goods and services.

With regard to the 6.3% reading, while energy costs did fall in April, they came back with a vengeance in May, which is too recent a development for this latest report to have captured with oil, natural gas, and diesel all posting new highs.

Meanwhile, China announced it will begin relaxing its COVID-zero policy starting on June 1, which should provide some relief to supply chain pressure, but will also likely renew upward pressure on commodity prices as their economy restarts, once again. In fact, Brent crude futures prices increased over the weekend in anticipation of this development and contracts are now trading above $120 a barrel, which is on course for a sixth straight monthly climb, the longest such run in more than a decade.

Elsewhere, on two separate occasions, the Biden administration was asked by the press corps whether they would consider curtailing or removing the tariffs on imported Chinese goods in an attempt to offer some price relief to US consumers. On both occasions, the answer provided was that this is something they are looking into. While we do see this as a potential net positive for the economy and overall market sentiment if this policy were pursued, and this would change the investing landscape, we cannot assign any meaningful probability to it happening.

State of the Market

Incredibly, we hardly hear anything about Ukraine lately, but the suffering created for the people of Ukraine and the damage the war has wracked to the global economy are still in place. With no end in sight, we continue to believe erroring on the side of caution is the prudent position to take.

Bigger picture, last month we spoke about managing your expectations for the market’s likely continued fragility and downside risk, and we were not wrong. To be clear, some healing occurred as a result of this latest bounce, but on a technical basis, still, most of the major asset classes around the world, remain below their 200-day moving average, which signals significant weakness remains. While the type of positive breadth we saw last week often precedes sustained rallies, most of the studies cited did not occur when the Fed was fighting inflation and trying to tighten financial conditions.

This type of broad weakness over a multi-month period is a rare occurrence, the most significant recent event being the Great Financial Crisis of 2008. Whether we will see more significant market weakness to come, or some crisis develop, we cannot know with certainty. However, we continue to recommend that investors keenly evaluate and budget their risk accordingly, especially on the back of last week’s rally.

To offer some perspective, as of June 1, the broad US market would need to rally roughly another 8% higher to regain its place above the 200-day moving average and reverse the downward trend that is in place.

On the back of last week’s rally, there now is a technical strength signal in US Large Value and High Dividend Equities, which are now trading above their 200-day moving average, and US Small Value is within striking distance, 2% below its moving average. But, on the whole, the weakness we are seeing is still quite pronounced across the globe.

While past history does not usually repeat itself perfectly, it’s been said it often does rhyme, and if we are to apply the lessons from other periods of a highly valued market or inflation (1929, the 1970s, and 2000) as roadmaps about the possibilities that lay ahead for the market presently, it was not unusual to have powerful relief rallies that still go on to make new lower lows, sometimes even after rallying for an extended period of time.

We could not agree more with Liz Ann Sonders, Chief Market Strategist at Charles Schwab,

“There is no perfect signal of when bear markets end. What we do know is that in bear markets, from a technical perspective, support becomes less relevant and resistance becomes more relevant. Assessing technicians’ consensus, as an example, resistance sits somewhere between 4330 and 4400 on the S&P 500, a range (for now) that represents a key hurdle. Although Friday brought a “volume thrust” (with higher volume associated with stronger stocks), historically persistent declines tend to end (or pause) with a string/series of positive breadth days. For now, rallies are more likely countertrend, while bouts of weakness are the trend.”

Her upper resistance target of 4330 is roughly 5% higher than today’s market close (6/1/22).

We think it’s also important to remember that the Federal Reserve’s mandate is not to stop the market from dropping, but we understand that investors may be conditioned to think that given the historic events it’s needed to intervene in over the last 15 years. Instead, one of the Fed’s mandates is to create price stability, and on that front, there’s much work to be done still and it will likely involve more pain in the market, and within our economy over the near term.

The Economy

Fortunately, as we’ve noted before, employment numbers remain robust, so for the Federal Reserve to serve its other mandate, full employment, the wind still is at our backs. The question is, is there strength to carry us through the shift that needs to occur with regard to inflation. The answer is, that no one knows.

Earlier in May, the Federal Reserve raised the target for the Fed Funds rate by half a point to 1% during its May 2022 meeting. This is the second consecutive rate hike and the biggest rise in borrowing costs since 2000.

The central bank added that ongoing increases in the target range will be appropriate, with Chair Powell pointing to 50bps hikes in “the next couple of meetings”, which indicates at least for now, a potential pause in September. Of course, not even Powell knows.

What we do know is that sentiment among the Federal Reserve Banking Committee is not on the same page, and rarely is. Over the long weekend, it was reported that voting FOMC member and Federal Reserve Governor Christopher Waller, was on the record while in Germany, saying, “I support tightening policy by another 50 basis points for several meetings.“

He continued, ”I am not taking 50 basis-point hikes off the table until I see inflation coming down closer to our 2 percent target. And, by the end of this year, I support having the policy rate at a level above neutral so that it is reducing demand for products and labor, bringing it more in line with supply and thus helping rein in inflation.”

What is especially important to note is that Waller has long been considered one of the doves of the committee, normally wanting to pursue low-interest rates and an accommodative policy. So, these days, if even he wants to be aggressive about stifling inflation, it is a very serious matter, indeed.

Looking ahead to the months ahead, the Federal Reserve will begin its Quantitative Tightening (QT) process, which will likely also create headwinds for equities.

Starting on June 1, the Fed will begin reducing its holdings of Treasury securities, agency debt, and agency mortgage-backed securities by a combined $47.5 billion per month for the first three months. Then in September, the total amount to be reduced goes up to $95 billion a month, with policymakers prepared to adjust their approach as the economy and financial markets evolve.

On the topic of what to expect from Quantitative Tightening, JP Morgan’s CEO, Jamie Dimon said, “You know, I said there’s storm clouds but I’m going to change it… it’s a hurricane. While conditions seem “fine” at the moment, nobody knows if the hurricane is a minor one or Superstorm Sandy. You better brace yourself. JPMorgan is bracing ourselves and we’re going to be very conservative with our balance sheet. We’ve never had QT like this, so you’re looking at something you could be writing history books on for 50 years.”

The goal of Quantitative Tightening is to raise yields and interest rates by removing liquidity, without raising the Fed Funds rate. That said, the reality is no one really knows what will happen with any certainty since we really are in truly uncharted waters. Put another way, results may vary.

Final Thoughts

Going into 2022, there were plenty of jokes dreading that this year would be like 2020, too. It has indeed been a very difficult year, and in our opinion, quite possibly one of the most difficult to navigate in over 20 years for investors. We are not alone in that viewpoint.

Goldman Sachs President, John Waldron said at an investor conference Thursday, “This is among — if not the most — complex, dynamic environments I’ve ever seen in my career. The confluence of the number of shocks to the system to me is unprecedented.”

In the face of these facts and data points, we continue to maintain a conservative outlook with downside concerns and reiterate that calm and patience will serve investors well.

That said, we are monitoring the markets and portfolios and we continue to be ready to make changes as necessary. As always, if you have any questions about your portfolio, feel free to contact us anytime. We’re here for you.